For years, financial professionals and managers have been using zero-based budgeting. It is a methodology that originated in corporate finance departments, and you can apply it to personal financial management.

This approach requires you to justify and allocate every rupee of income each month. It is different from traditional budgeting methods that adjust previous spending patterns.

Households across India have looked for ways to manage their finances better. Economic uncertainty, rising living costs, and a focus on financial independence have pushed this change.

While regular budgeting systems use past spending as a starting point, zero-based budgeting begins each month with a zero balance. In this article, we will cover all you need to know about zero-based budgeting.

The Corporate Origins and Core Principles of Zero-based Budgeting

Zero-based budgeting started in the corporate sector during the 1970s. Texas Instruments manager Peter Pyhrr developed this method as an alternative to regular budgeting. The system got attention when Jimmy Carter, then Governor of Georgia, used it across state government operations. He brought this approach to federal budgeting during his presidency.

The main idea requires that every expense must be justified for each new period. You cannot simply look at previous budgets and make changes. In corporate use, department managers must build their budgets from zero each fiscal year. They must defend each line item regardless of whether it appeared in previous budgets. This process removes the assumption that past spending should continue.

How It Works for Personal Finances

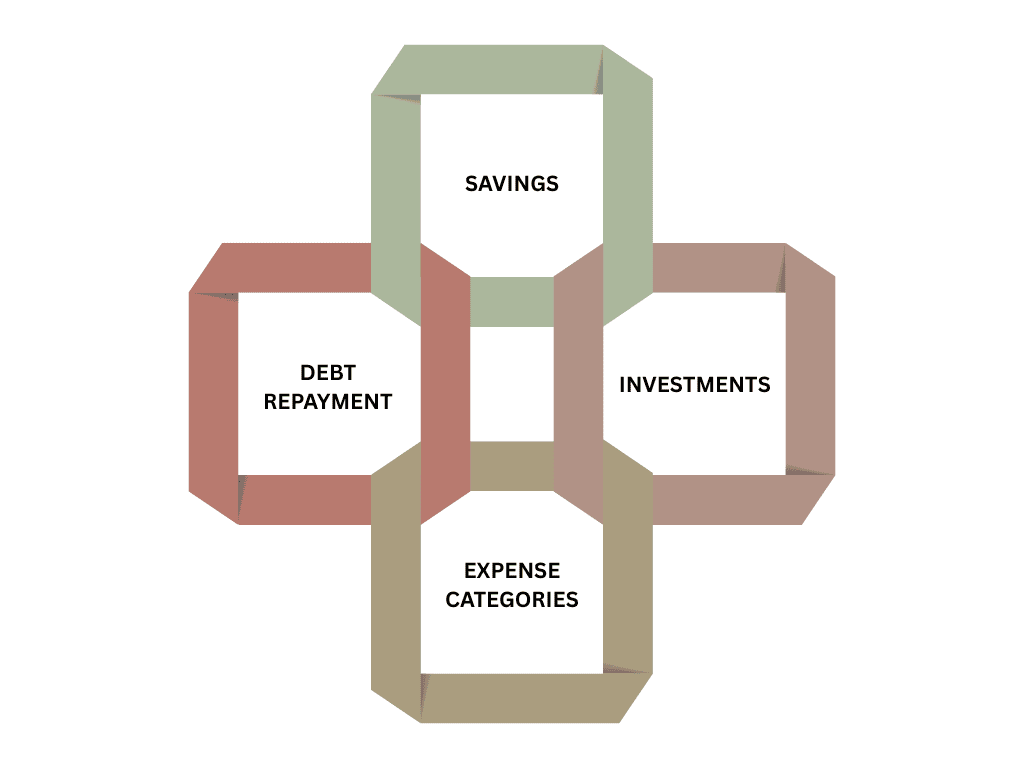

You can apply this to your personal finances on a similar basis. You assign every rupee of monthly income to different categories. These include:

You continue until the balance reaches zero. This does not mean spending all your money. It means every rupee has a purpose, including amounts you put in savings and investment accounts.

How to Start Zero-Based Budgeting

The first step begins with calculating the total monthly income from all sources.

Step 1: Calculate Your Total Monthly Income

The first step begins with calculating the total monthly income from all sources. This includes:

Salary

Investment returns

Rental income

Any other income streams

You must count net income. That is the amount you get after tax deductions, not gross salary figures.

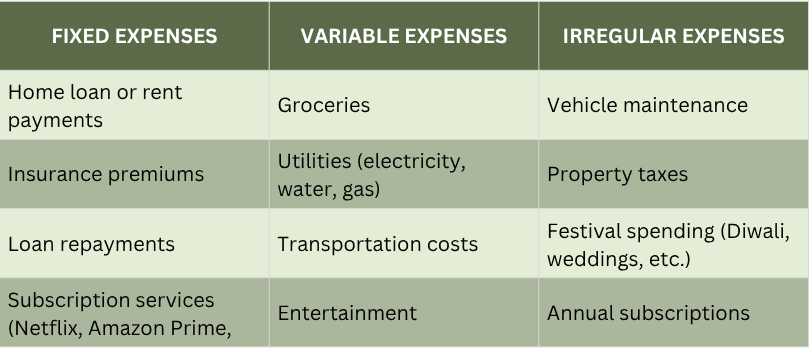

Step 2: List All Your Expenses

After calculating income, you need to list all monthly expenses and financial obligations.

Step 3: Allocate Every Rupee

The main difference from traditional budgeting shows up in how you allocate money. You cannot guess expenses based on previous months. You cannot let money sit in your savings account without a plan. Zero-based budgeting requires you to assign amounts to each category until total allocations equal total income. Financial planners call this "giving every rupee a job."

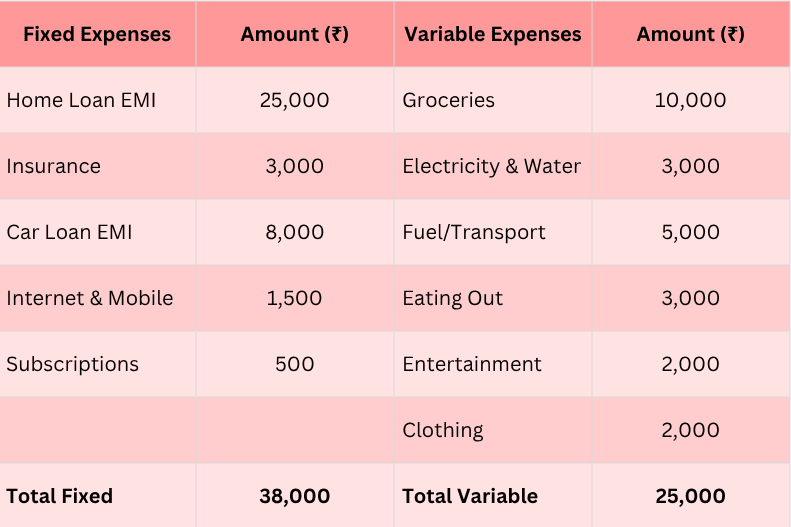

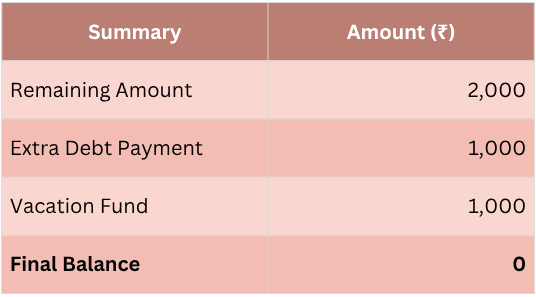

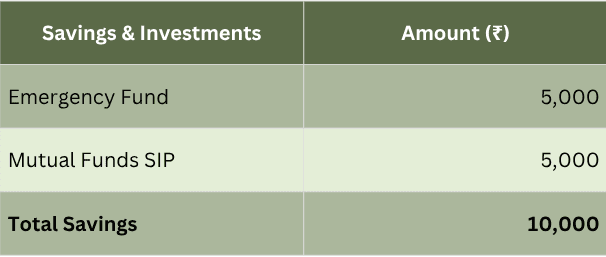

Let us say Rajesh earns ₹75,000 per month after taxes. Here is how he would do zero-based budgeting:

Income: ₹75,000

Benefits of Zero-based Budgeting for Your Money Management

This method offers real benefits for managing your personal finances.

Increased Awareness

This method offers real benefits for managing your personal finances. The need to justify and allocate every rupee makes you more aware of your spending patterns and money priorities. This planning process often shows you expenses that you might not have noticed or questioned with regular budgeting.

Stops Mental Accounting Errors

Financial advisors say that zero-based budgeting stops what economists call "mental accounting errors." These happen when you treat money differently based on where it came from or what you plan to use it for. You should see all money as resources that need smart planning. The system forces you to make decisions about every rupee. It cuts down on impulse spending and makes you more thoughtful about your money choices.

More Flexibility

This approach also gives you more flexibility than traditional budgeting methods. Each month starts with a fresh planning process. You can change spending categories to match changing situations, priorities, or expenses.

For example:

Summer months: More money for electricity bills, less for clothing

Festival months: More for gifts and celebrations, less for entertainment

Medical emergency: More for healthcare, less for eating out

You do not just go over a fixed budget line. You adjust other categories to balance it out.

Better Financial Results

Households using zero-based budgeting usually save more money and pay off debt faster. The clear assignment of money to savings and debt repayment makes the difference. You treat these as must-pay expenses rather than what is left over. This leads to better money outcomes.

Challenges You Might Face Using Zero-based Budgeting

Zero-based budgeting has some challenges that you must handle for it to work.

Time and Effort Required

Zero-based budgeting has some challenges that you must handle for it to work. This method needs more time and effort than traditional budgeting. This is especially true when you start. Making detailed expense categories, tracking actual spending against plans, and changing categories during the month needs regular attention and record-keeping.

Variable Income Problems

You face more difficulty if your income changes a lot. This includes:

Self-employed people

Commission-based sales workers

Freelancers

Those with seasonal jobs

The system works best with steady income that lets you plan each month accurately. Those with changing income must either budget based on the lowest income or use other methods. Budgeting on minimum income creates problems during months when you earn more. Averaging income over longer periods is another option.

Feels Restrictive

The mental shift needed for zero-based budgeting also creates challenges for some people. The system's strict approach to money control can feel limiting. This is true if you are used to more flexible spending habits. Financial psychologists say that making it work often needs you to think about the method differently. You should see it not as limiting but as freeing. It gives you clear permission to spend planned amounts rather than putting up barriers.

Coordination in Families

Couples and families using zero-based budgeting must also work through the challenges of managing money together. The system needs agreement on priorities, how to allocate money, and spending within categories. Financial counsellors suggest regular budget meetings. Family members should make monthly plans together. This makes sure everyone understands and commits to the plan.

The Bottom Line

Zero-based budgeting's effects go beyond just controlling spending now. The money awareness you build through regular planning affects broader money habits. These include paying more attention to investment performance, smarter debt management, and better long-term financial planning.

The process needs ongoing discipline and has real potential for money improvement. Zero-based budgeting works as a practical tool if you commit to getting better money control. It speeds up progress toward your money goals.