Managing your personal finances effectively can be overwhelming. But what if we tell you that just three financial ratios can give you a clear picture of your financial health?

Among numerous indicators, three financial ratios stand out as essential tools for evaluating your financial health: the Savings Rate, the Emergency Fund Ratio, and the Debt-to-Income Ratio. These ratios provide a simple way to assess your financial stability and independence. Let’s get into the details.

1. The Savings Rate

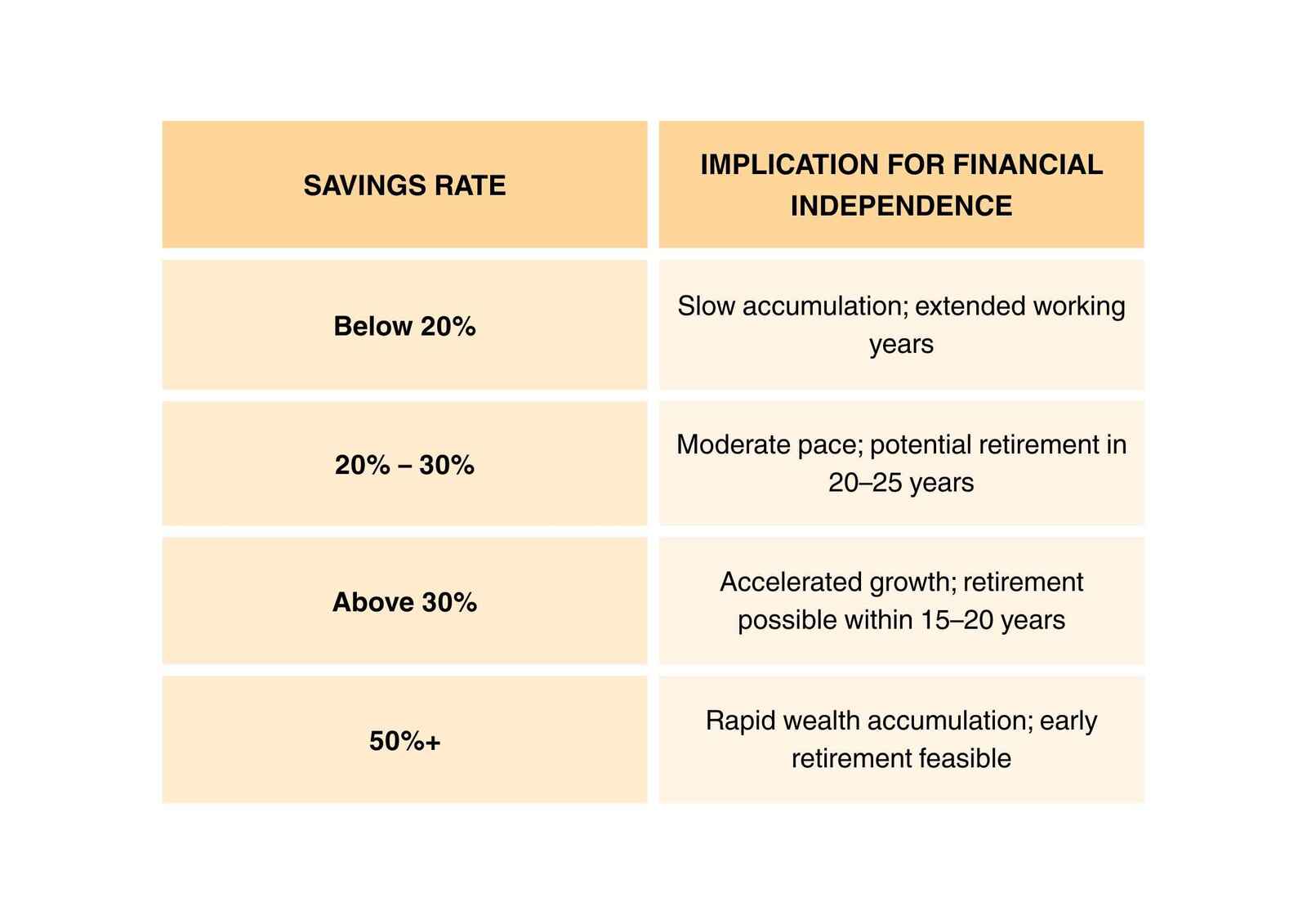

The savings rate is the percentage of your income that you save and invest. Unlike absolute savings amounts, this percentage provides a more meaningful measure for wealth accumulation.

Your savings rate affects how quickly you can reach financial independence. Reaching important milestones like 20%, 30%, or even 50% savings can speed up your path to financial freedom.

For instance, a savings rate above 30% can significantly shorten the time required to accumulate sufficient assets for retirement.

Consider an individual earning ₹60,000 monthly who saves ₹15,000. Their savings rate is 25%, positioning them well on the path to financial independence.

How to Calculate Your Savings Rate

Savings Rate = ((Monthly Savings + Monthly Investments) ÷ Monthly Income) × 100%

If your monthly income is ₹60,000 and you save ₹15,000 monthly, your savings rate is:

₹15,000 ÷ ₹60,000 × 100 = 25%

This means you're saving 25% of your income.

2. The Emergency Fund Ratio

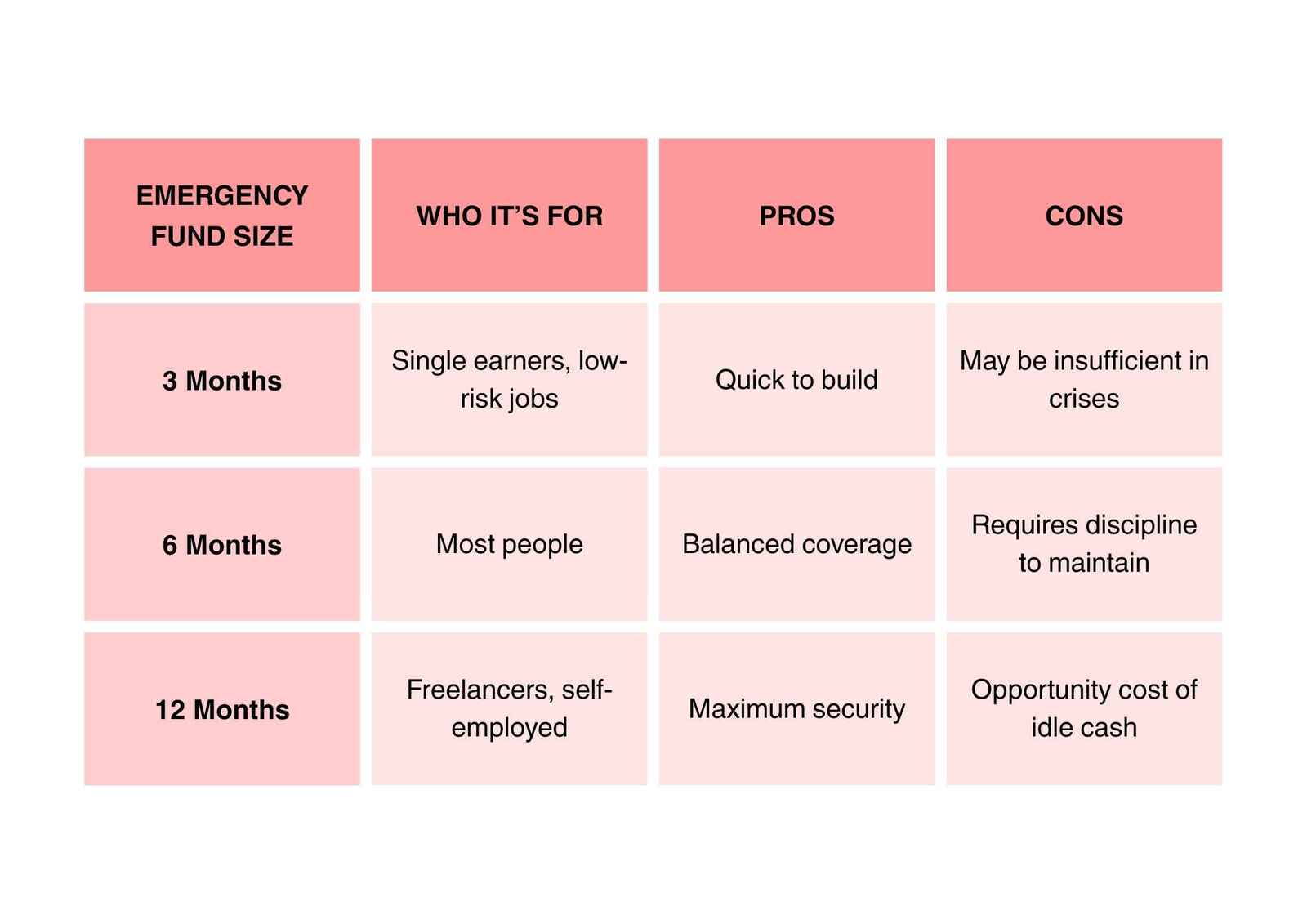

Your emergency fund ratio shows how many months you can pay for essential expenses if your income stops. It acts as your financial safety net.

The 3, 6, 12 Month Debate

How to Calculate Your Emergency Fund Ratio

Emergency Fund Ratio = Emergency Fund Amount ÷ Monthly Essential Expenses

If you have ₹1,80,000 saved and your essential monthly expenses are ₹30,000:

₹1,80,000 ÷ ₹30,000 = 6 months

This means your emergency fund would last you 6 months.

3.The Debt-to-Income Ratio

This ratio shows how much of your monthly income goes to paying off debts. It’s a key measure of financial stress and borrowing capacity.

How to Calculate Your Debt-to-Income Ratio

DTI Ratio = (Monthly Debt Payments ÷ Monthly Income) × 100

Example:

₹24,000 ÷ ₹80,000 × 100 = 30%

This means 30% of your income is committed to debt payments

Home loans often dominate your DTI. Since housing is a necessity, lenders allow higher DTI limits if a big chunk is home loan EMI. But it’s important to adjust your calculations to reflect your comfort level.

Reducing your DTI by just 5 percentage points can significantly increase your financial flexibility. For example, lowering your DTI from 40% to 35% frees up ₹4,000 per month on an income of ₹80,000.

Putting It All Together: Your Financial Health Scorecard

A single metric doesn't define your financial health. It's a complete picture formed by multiple ratios working together. Understanding how these ratios interact provides you with a framework for assessing your financial stability.

The Balance Between Ratios

These financial ratios work together instead of being separate measures. When you improve one ratio, it usually helps the others as well. For example, if you raise your savings rate from 15% to 20%, you strengthen your ability to save for an emergency fund and lower your need for debt. Also, if you keep your DTI ratio at 25% instead of 35%, you will have more money available to save or invest.

This means strategic improvements in one area can provide benefits across your entire financial profile.

The Monthly Check-In

Effective financial management means keeping an eye on your finances without becoming obsessed. A simple 5-minute review each month gives you enough oversight without making it a chore.

During this review, compare your current metrics against established benchmarks:

Record these values consistently to establish trend lines rather than focusing on individual data points. Temporary fluctuations matter less than directional movement over quarterly and annual periods.

The Improvement Hierarchy

Financial stability follows a logical progression. Each level builds upon the previous foundation:

Start with the Savings Rate: It is key to your financial health. Without saving regularly, your financial goals will stay dreams instead of becoming reality. Set up automatic transfers on payday to make saving consistent. Even a small increase, like 1%, can grow a lot over time. If your savings rate is below 10%, make it your priority to raise it to at least 15% before focusing on other financial goals.

Build Emergency Fund: Once you have a good savings habit, set aside some money for an emergency fund. This savings will help you handle small setbacks without affecting your overall financial goals. Begin by saving enough to cover one month of expenses, and then work towards saving enough for 3 to 6 months. Keep this fund separate from your regular checking accounts so you are not tempted to use it for everyday spending.

Reduce Debt: With savings established and a basic emergency fund in place, accelerated debt reduction becomes sustainable. Prioritise high-interest debt first while maintaining minimum payments on all obligations. Reducing the DTI ratio by one percentage point improves financial flexibility and lowers the risk of facing problems during economic downturns.

The Progress Tracking Method

Effective tracking balances awareness with practicality. Here are three approaches for you:

Visual Representation: Use simple line graphs to show each ratio over 12 to 24 months. This makes it easier to see patterns that you might not notice with just numbers.

Milestone Recognition: You can set specific goals, such as building a 3-month emergency fund or lowering your DTI ratio below 30%. Celebrate these achievements formally instead of letting them go unnoticed.

Quarterly Deep Reviews: While monthly checks keep you aware, quarterly reviews allow for deeper analysis. Take time to look not just at the numbers but also at what affects them. Has your income gone up? Have your essential expenses changed? Have you taken on new debts?

This approach turns financial concepts into useful tools for tracking your progress.

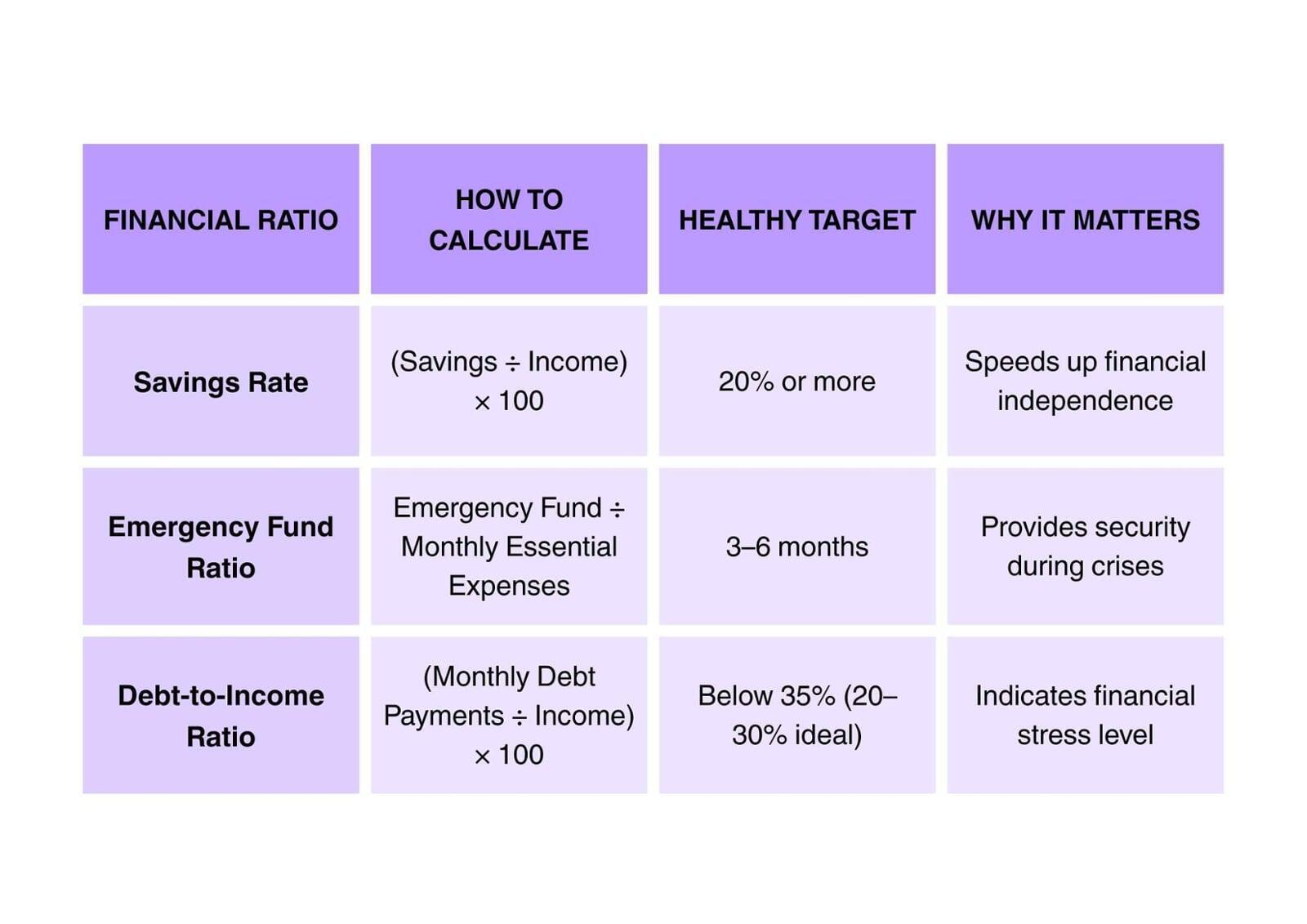

Summary of Key Ratios and Targets

Conclusion

Focusing on just these three financial ratios gives you a clear, actionable picture of your financial health. The savings rate shows how fast you’re building wealth. The emergency fund ratio tells you how prepared you are for the unexpected. The debt-to-income ratio reveals how much financial pressure you’re under.

By tracking and improving these numbers, you can take charge of your finances, lower your stress, and make steady progress toward financial freedom. Remember, it’s about making progress, not being perfect. Start today and see how these simple ratios can change your financial life.