Buying a home is one of the biggest financial decisions you will make in your life. Most people in India take a home loan to buy their property. But here is a question that confuses many buyers.

Should you take a 15-year home loan or a 30-year home loan?

The loan tenure you choose affects your monthly EMI, total interest paid, and overall financial health.

Let us look at both options in detail. We will compare the costs, benefits, and situations where each works best. This will help you make an informed decision for your financial planning.

Understanding Home Loan Tenure in India

Loan tenure is the time period you take to repay your home loan. In India, most banks and housing finance companies offer home loans with tenures ranging from 5 years to 30 years. The two most popular options are 15-year and 30-year tenures.

The tenure you choose directly affects three things. First is your monthly EMI amount. Longer tenure means lower EMI, shorter tenure means higher EMI. Second is the total interest paid. Longer tenure means more interest, shorter tenure means less interest. Third is your financial flexibility. Longer tenure gives more monthly cash flow, shorter tenure builds equity faster.

Most Indian home buyers prefer longer tenures. The average home loan tenure in India is around 20-25 years. This is because longer tenures keep EMIs affordable.

The 15-Year Home Loan: A Clear Picture

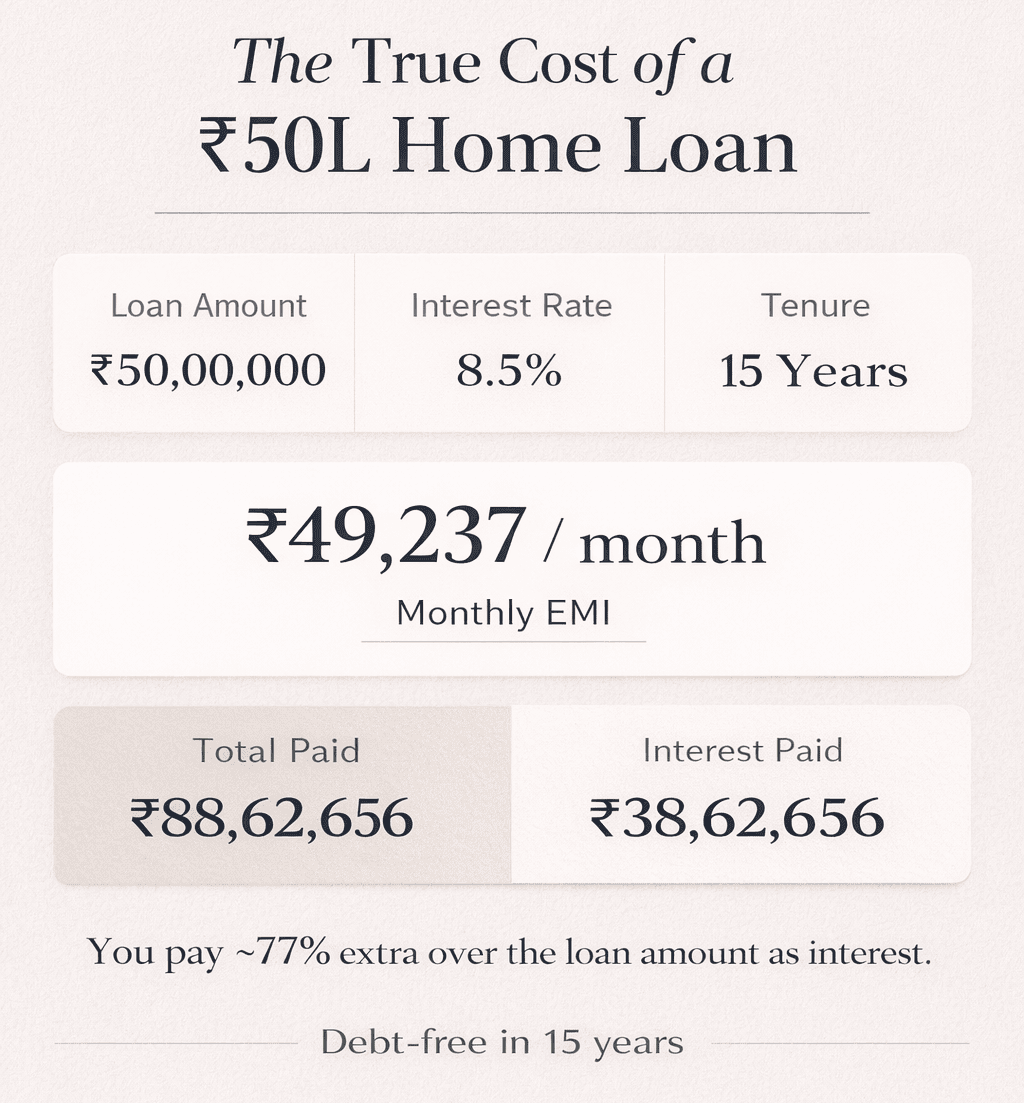

A 15-year home loan means you repay your entire loan in 15 years or 180 monthly instalments. The EMI is higher compared to a 30-year loan for the same amount. But you pay much less interest overall.

Let us say you take a home loan of ₹50 lakhs at 8.5% interest rate. With a 15-year loan, your monthly EMI would be ₹49,237. The total amount you pay over 15 years is ₹88,62,656. The total interest you pay is ₹38,62,656. You become debt-free in 15 years.

Your monthly payment is significantly higher with a 15-year loan. It requires a stable and higher income. You will have less money left for other expenses each month. But the benefit is that you pay much less interest over the loan period. The interest component in your EMI reduces faster. The total cost of the home is lower.

High income earners should consider a 15-year loan. If you earn well and can afford higher EMIs, this works for you. Your monthly income should be at least 4-5 times the EMI. You should have job stability.

The 15-Year Home Loan: A Clear Picture

A 15-year home loan means you repay your entire loan in 15 years or 180 monthly instalments. The EMI is higher compared to a 30-year loan for the same amount. But you pay much less interest overall.

Your monthly payment is significantly higher with a 15-year loan. It requires a stable and higher income. You will have less money left for other expenses each month. But the benefit is that you pay much less interest over the loan period. The interest component in your EMI reduces faster. The total cost of the home is lower.

High income earners should consider a 15-year loan. If you earn well and can afford higher EMIs, this works for you. Your monthly income should be at least 4-5 times the EMI. You should have job stability.

The Big Advantage: Interest Savings

The massive interest savings are the biggest advantage. You save lakhs of rupees in interest. More of your money goes to owning the home. The total cost of ownership is lower.

You become debt-free faster with a 15-year loan. You own your home in half the time compared to a 30-year loan. You have no loan burden in your 50s. You get financial freedom earlier in life.

The Main Challenge: High Monthly Burden

The high monthly burden is the main disadvantage. The EMI takes a big chunk of your monthly income. You have less money for other expenses. It can strain your budget significantly. You have less financial flexibility with a 15-year loan.

Your cash flow is limited for emergencies. It becomes difficult to invest in other opportunities.

The 30-Year Home Loan: A Detailed Look

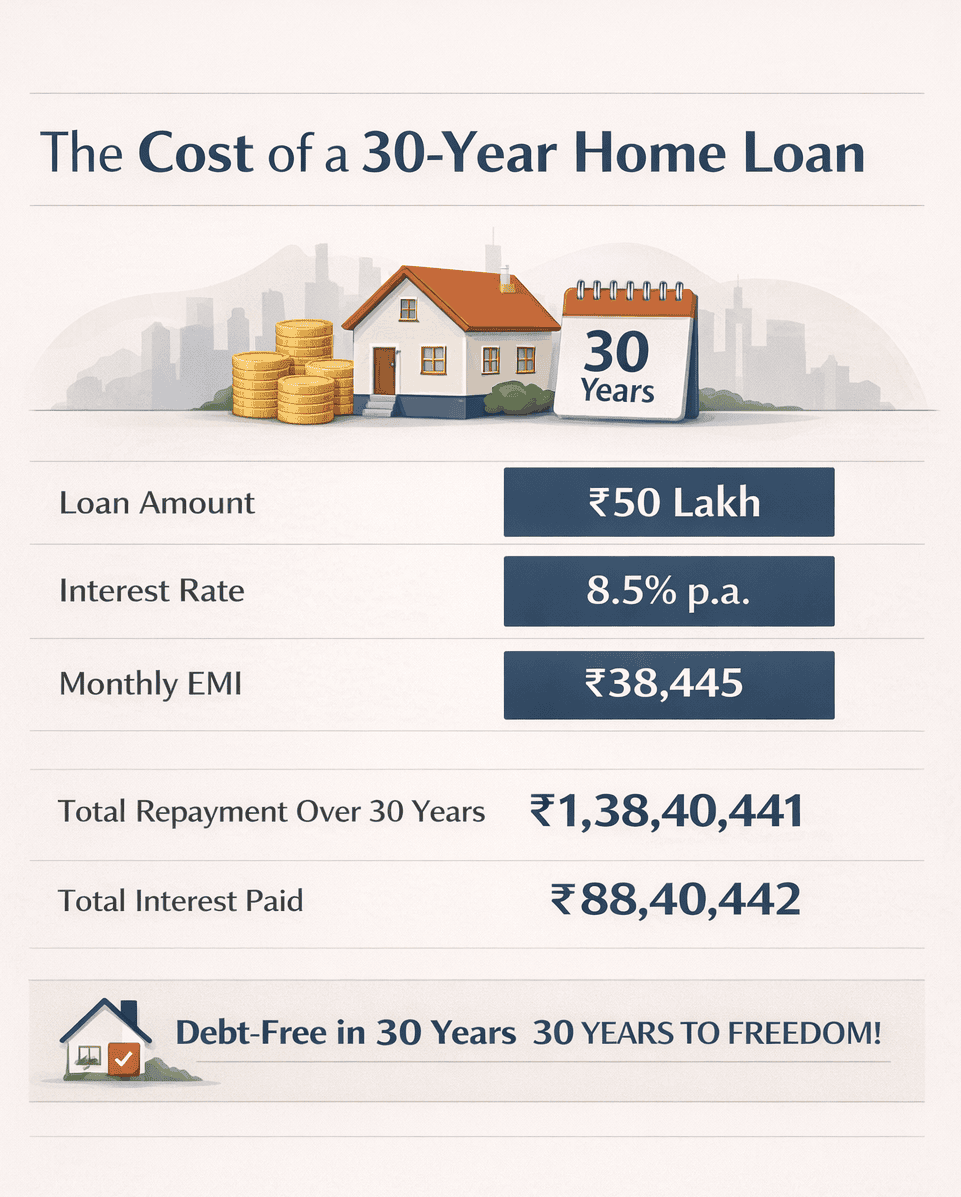

A 30-year home loan means you repay your entire loan in 30 years or 360 monthly instalments. The EMI is much lower compared to a 15-year loan for the same amount. But you pay significantly more interest overall.

Now compare this with the 15-year loan. The EMI difference is ₹10,792 less per month. But the interest difference is ₹49,77,786 more over the loan period. The time difference is 15 years longer to become debt-free. You pay almost ₹50 lakhs more in interest with a 30-year loan. But you save ₹10,792 every month.

Moderate income earners may consider a 30-year loan. If your income is moderate and growing, this may work better. Those with multiple financial goals benefit from 30-year loans. If you have children's education to plan for, you need cash flow. If you want to invest in other assets too, you need flexibility. If you need money for emergencies and lifestyle expenses, a lower EMI helps.

The Key Benefits: Flexibility and Cash Flow

Affordable monthly payments is the primary advantage. The EMI is much lower and manageable. It does not strain your monthly budget. It is easier to qualify for the loan. Better cash flow is another major benefit. You have more money available each month.

You can invest in mutual funds, stocks, or PPF. You can build an emergency fund simultaneously.

Higher loan eligibility comes with 30-year loans. Banks approve higher loan amounts because the EMI is lower. You can buy a better property. It is easier to get loan approval. Financial flexibility is a key advantage. You can handle income disruptions better. You have money available for emergencies. You can maintain your lifestyle quality.

The Major Drawback: Huge Interest Cost

The huge interest burden is the biggest disadvantage. You pay almost double the interest compared to a 15-year loan. The total cost becomes very high. Much more of your money goes to the bank instead of building your wealth.

You carry debt for a longer period with a 30-year loan. You have a loan burden for 30 years. You may still have a loan during retirement.

Making the Right Choice for Your Situation

Your age and career stage matter a lot. If you are in your 20s, a 30-year loan makes more sense. Your income will grow significantly over the next decade. You have time to prepay later. If you are in your 30s, consider a 15-20 year loan. You may have a stable income now. You want to be debt-free before 50. If you are in your 40s, a 15-year or shorter loan can make you debt-free quicker as you approach retirement.

Your income stability is also crucial. If you are salaried with a stable job, you can consider a 15-year loan. Your income is predictable. However, if you are a business owner or freelancer, a 30-year loan is safer. Your income fluctuates month to month. You need flexibility for lean months.

Lastly, your other financial goals need consideration. If you have children's education to plan for, a 30-year loan is better. Education costs are high and certain. You need cash flow for school fees. If retirement planning is important and retirement is 20+ years away, a 15-year loan works. If retirement is 10-15 years away, choose carefully.

The Middle Path: Hybrid Strategies

You do not have to choose between 15 and 30 years strictly. You can take a 30-year loan for lower EMI and prepay aggressively whenever you have extra money. Use bonuses, increments, and windfalls for prepayment. You can reduce tenure to 15-20 years through prepayments. This gives you the flexibility of lower EMI and a safety net during tough times. You get interest savings through prepayments and can adjust based on your financial situation.

Another option is to take a 20-year loan as a middle ground. For a ₹50 lakh loan at 8.5%, your monthly EMI would be ₹43,391. Total interest paid would be ₹54,13,878. You become debt-free in 20 years. It is more affordable than a 15-year loan. It costs less interest than a 30-year loan. It gives you a reasonable timeline to debt freedom.

Some banks offer a step-up EMI facility. You start with lower EMI that increases by 5-10% annually. This matches your expected income growth. It reduces overall interest compared to a flat 30-year loan. It is affordable in the early years and automatically increases with your income.

The Bottom Line

There is no universal answer to the 15-year vs 30-year debate. Your choice depends on your unique situation.

The key is to be intentional about your choice. Calculate the numbers. Understand the trade-offs. Choose what works for your life stage and financial situation and most importantly, stick to your plan.