Life is unpredictable. Just when you think your financial plan is solid, an unexpected event can shake everything up.The COVID-19 pandemic, the 2008 global financial crisis, or sudden job losses are examples of what is called “Black Swan” events.

They are rare, unforeseen incidents that have a massive impact. These events test your financial resilience like nothing else.

So, how prepared is your financial plan for the next big shock? Can it handle sudden income loss, market crashes, or unexpected expenses? Stress-testing your financial plan is the answer. It means putting your plan through tough scenarios to see if it holds up. If it doesn’t, you fix the weak spots before disaster strikes.

In this article, we will explore what stress-testing your financial plan means, why it is critical, and how you can do it effectively. We will also look at common risks, practical steps to strengthen your plan, and how to stay ready for whatever comes next.

What Is Stress-Testing Your Financial Plan?

Stress-testing is a way to simulate extreme but plausible scenarios to check how your finances would react. Think of it like a fire drill for your money.

You imagine situations like losing your job for six months, a stock market crash wiping out half your investments, or a major medical emergency. Then, you analyse how your income, expenses, savings, and investments would hold up.

The goal is to find vulnerabilities before they become real problems. If your plan fails the test, you identify what needs fixing, whether it’s building a bigger emergency fund, diversifying investments, or reducing debt. Stress-testing helps you move from hope to preparation.

Why Stress-Testing Matters More Than Ever

The last decade has shown us how quickly the world can change. The pandemic shut down economies overnight. Markets crashed and then bounced back unpredictably. Millions lost jobs or faced pay cuts. Inflation surged. Political tensions created uncertainty.

If your financial plan was rigid or based on best-case assumptions, you might have struggled. Stress-testing forces you to think beyond the usual and prepare for the worst. It builds confidence that your plan can survive shocks and keep you on track.

For Indians, this is especially important. Our economy is growing but remains vulnerable to global shocks, policy changes, and natural disasters. Many households rely on a single income source or have limited savings. Stress-testing can reveal gaps that you might not see otherwise.

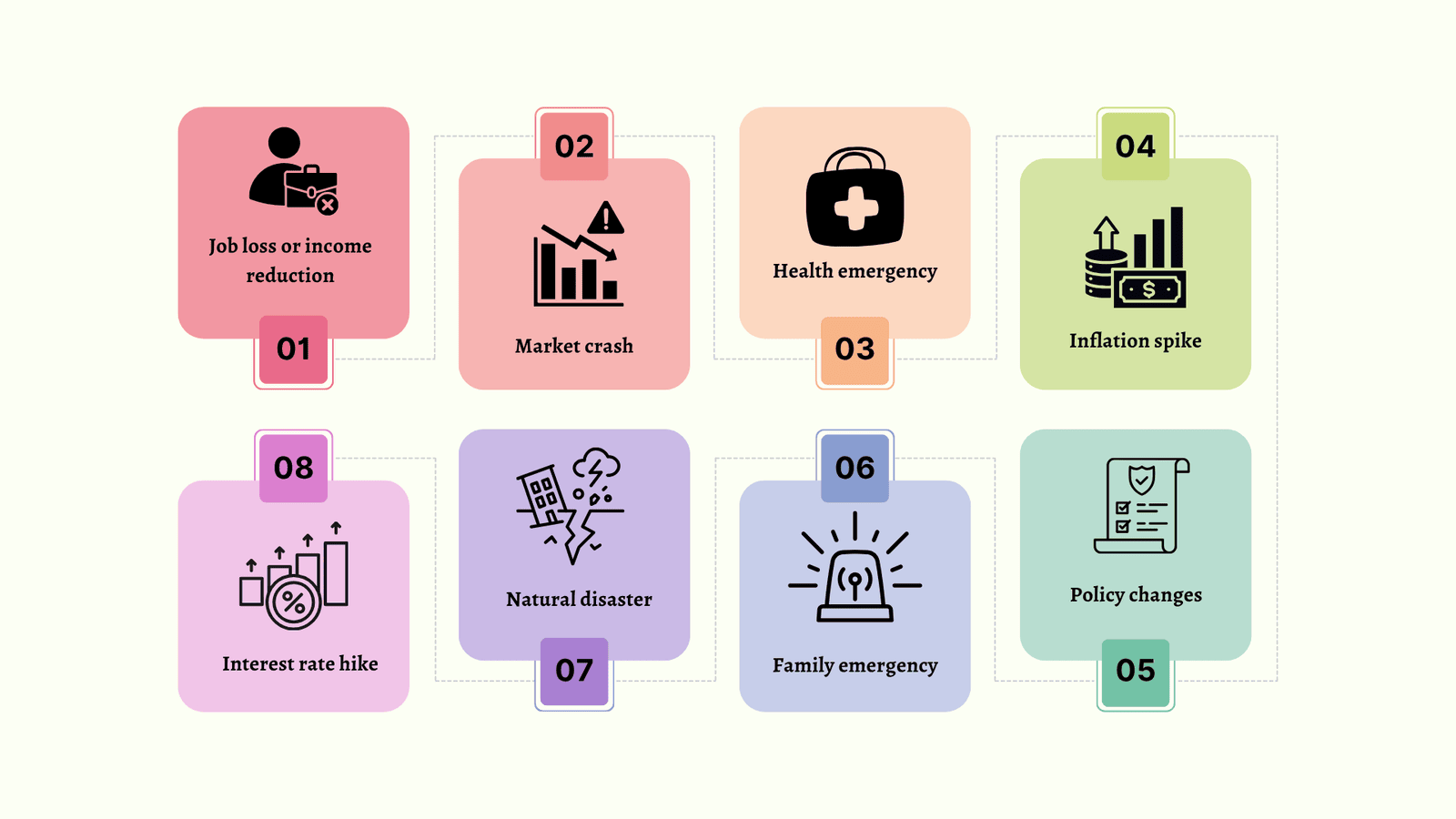

Common Risks to Include in Your Stress-Test

When stress-testing, consider risks that could realistically affect you. Here are some common ones:

Job loss or income reduction: Losing your main source of income for 3-12 months.

Market crash: A sudden 30-50% drop in your investment portfolio.

Health emergency: Major medical expenses not covered by insurance.

Inflation spike: Rapid rise in prices increasing your monthly expenses.

Interest rate hike: Higher loan EMIs due to rising interest rates.

Natural disaster: Damage to property requiring large repairs or relocation.

Family emergency: Unexpected financial support needed for relatives.

Policy changes: Tax law changes or subsidy cuts affecting your finances.

You don’t need to include every risk, but pick those most relevant to your situation.

How to Stress-Test Your Financial Plan: Step-by-Step

Here is a step-by-step guide.

Step 1: List Your Financial Components

Start by listing all parts of your financial plan:

Income sources (salary, business, investments)

Monthly expenses (fixed and variable)

Savings and emergency fund

Investments (stocks, mutual funds, real estate)

Debts and loans

Insurance coverage

Having a clear picture helps you understand what might break under pressure.

Step 2: Create Worst-Case Scenarios

Imagine what would happen if one or more risks hit at the same time. For example:

You lose your job, and the stock market drops 40%.

Your medical emergency costs ₹5 lakhs, and inflation rises by 10%.

Your loan EMI increases by 20% due to interest rate hikes while your income drops.

Write down these scenarios with numbers. Be realistic but conservative.

Step 3: Calculate the Impact

For each scenario, calculate:

How long your emergency fund can cover expenses.

How much income you would lose and for how long.

How much your investments would lose in value.

How your monthly budget would be affected.

Whether you can still meet loan payments and other obligations.

Use spreadsheets or financial apps to help with calculations.

Step 4: Identify Weaknesses

Look for areas where your plan fails. For example:

Your emergency fund lasts only 2 months but you might be unemployed for 6.

Your investments lose half their value and you panic-sell at a loss.

Your monthly expenses exceed your reduced income.

You have no health insurance or inadequate coverage.

Your debt payments are too high to manage if income drops.

These are your weak spots that need fixing.

Step 5: Make a Plan to Fix Them

Once you know the gaps, take action:

Build your emergency fund to cover at least 6-12 months of expenses.

Diversify your investments to reduce risk.

Cut unnecessary expenses to lower your monthly burn rate.

Increase insurance coverage for health, life, and property.

Pay down high-interest debt aggressively.

Create alternative income streams or backup plans.

Review and update your financial plan regularly.

Practical Tips to Strengthen Your Finances

Let’s look at some tips now.

Build an Emergency Fund

An emergency fund is your first line of defence. Ideally, it should cover 6-12 months of essential expenses. Keep it in a liquid and safe place like a savings account or liquid mutual fund. Avoid investing this money in volatile assets.

Diversify Your Investments

Don’t put all your eggs in one basket. Spread your investments across asset classes, equity, debt, gold, real estate, and sectors. Diversification reduces the impact of any single market crash. However, talk to a financial advisor to get more clarity.

Manage Debt Wisely

High-interest debt drains your finances and adds stress. Pay off credit card balances and personal loans quickly. Avoid taking on new debt unless necessary. If you have home loans or other EMIs, consider tenure and interest rates carefully.

Maintain Adequate Insurance

Insurance protects you from financial shocks. Have term life insurance to cover your family’s needs. Health insurance is a must to avoid crippling medical bills. Consider critical illness and disability insurance if possible.

Plan for Income Disruptions

If your income depends on one source, think about alternatives. Freelancing, part-time work, or passive income streams can help. Keep your skills updated to improve job security.

Regularly Review Your Financial Plan

Life changes, and so should your plan. Review it at least once a year or after major events. Update your goals, budgets, and investments accordingly.

How to Stay Calm During a Black Swan Event

Stress-testing prepares your finances, but it also prepares your mind. When a crisis hits, panic can lead to poor decisions, such as selling investments at a loss or taking on high-interest loans.

Stay calm by:

Remembering your plan and the buffers you built.

Avoiding rash financial moves.

Consult your financial advisor before making big changes.

Focusing on long-term goals, not short-term market swings.

Conclusion: Is Your Financial Plan Ready?

Stress-testing your financial plan is not a one-time task. It is an ongoing process that keeps you ready for whatever life throws at you. By imagining worst-case scenarios and fixing weaknesses, you build confidence and resilience.

If you haven’t stress-tested your plan yet, start today. The next Black Swan event may come when you least expect it. Will your financial plan hold strong or crumble? The choice is yours. Prepare now, so you can face the future with strength and peace